All Categories

Featured

Table of Contents

By doing this, you will not affect your available credit, but you will ensure nobody else can attempt to use it either, Mandy kept in mind. It's simple to think of a budget plan as a lorry to restrict enjoyable, but developing a spending plan will help you say "yes" in the future to the things and experiences you truly desire.

"Update that budget plan and verify what your regular monthly costs are really like make certain none have increased without your understanding," Mandy said.

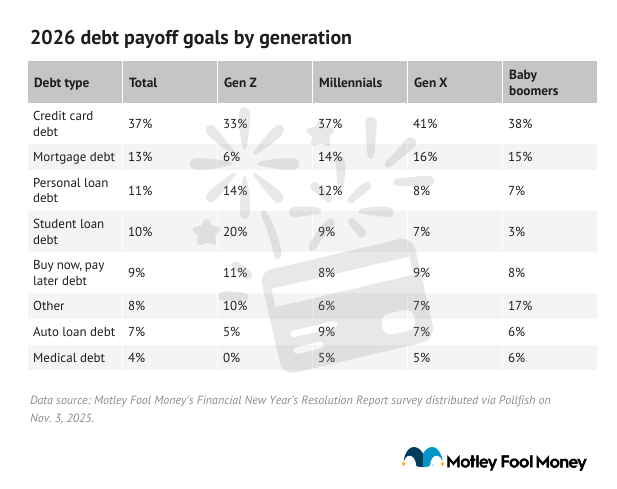

Possibly your resolution for 2026 is to pay down financial obligation, start your retirement savings, or conserve for a huge ticket item. Perhaps you need assistance with individual financing however do not understand where to start. In any case, prioritizing your objectives for the New Year comes down to understanding what you value the most, Kumiko Love, a certified monetary counselor and author of "My Cash, My Way," told PBS News.

Of the 30% of Americans who state they make a minimum of one resolution, 61% say they are concentrated on cash or finances, according to Seat Research. And a bulk of Americans 87% say they achieve at least some of their annual resolutions. To Love, drawing up small wins along the way can help you remain the course.

"The honest fact is we live more in our everyday than at our outcome." To assist you set yourself up for monetary success this year, PBS News asked experts for pointers on reaching various financial objectives. Fear around your cash "many of the time comes from the unidentified," Love said.

Ways for Preparing Your Finances in 2026

You're really nervous and worried out because you have no idea what's going on with your cash," echoed Tori Dunlap, a self-taught cash and profession specialist who founded the monetary education platform Her First 100K. When you sit down to look at the numbers, "rewire all of that shame and the fear and the guilt you feel," suggested Dunlap, author of "Financial Feminist.

Choosing the Top Rewards Cards in 2026"The most crucial thing in this day and time is that if you feel overloaded, if you feel burdened, that you reach out and state, 'I need assistance,'" stated Michelle Singletary, personal finance columnist at The Washington Post. She suggests checking out personal finance classes or community programs, or finding a responsibility partner.

"This is not a blame video game," Love said.

Rebuilding Damaged Rating Ratings Quickly for 2026

"Charge card debt always is going to have a high rate of interest. That's probably the financial obligation you need to work to remove first before you worry about your lesser interest debt," Dunlap stated. If you have several charge card with various interest rates, begin with the one with the greatest interest rate.

It's very high and it compounds every day," Dunlap informed PBS News. "So, every day you invest in debt, it gets more costly. Personal loans allow you to typically secure a loan at a lower rates of interest with one single monthly payment that isn't going to compound every day." The personal loan path to pay off high-interest credit card financial obligation can be "a nice reset for your cash." Dunlap said the method for paying off your trainee loan debt depends upon what sort of loans they are and what the rates of interest is.

You might receive an income-based repayment plan that could help offer you "some breathing space" to focus on whatever debt is most eating into your cash circulation and ruining your spending plan, she included. Dunlap shared what she calls the "7 to 8% rule." If the rates of interest on your trainee loan financial obligation is more than 7 to 8%, then it costs you more money to be in financial obligation, so you need to pay it off faster.

Perfecting Your Future Budget Plan

If the interest rate is less than that, Dunlap suggests sticking with month-to-month payments and focusing on investing any additional earnings rather. If you have private trainee loans at a high rates of interest, Dunlap stated it might be worth refinancing, but she stated "do not take your federal loans private." "That takes you out of potential trainee loan forgiveness in the future," Dunlap stated, and won't allow you to get on an income-based payment strategy.

"It must be safe, consistent, and over a long duration of time." She said day trading or picking "a hot stock" is extremely risky. The top place to begin when investing is utilizing your pension to its complete advantage, both Dunlap and Love stated. "Investing ought to not be attractive." "Individuals do not understand that pension like a 401k or an IRA are investing accounts and they're tax advantaged, meaning that the federal government is incentivizing you to conserve for your retirement by offering you tax breaks," Dunlap said.

"It's like free money" you can use to invest. Otherwise, you'll spend "years in what I call monetary purgatory," Dunlap stated.

That's what they're there for," Love said Love stressed that while she is a recognized monetary therapist, she is not a fiduciary. Her suggestions should not take the place of recommendations from an advisor with particular details about your properties. There are three steps that come to mind for how you might start "upping your retirement game." "start with your [ company] match." If you want to go above and beyond, "I would move to a Roth IRA or standard Individual retirement account, depending on your tax bracket and where you're gon na be in retirement." And after that "I [would] take a look at something called a health cost savings account," where individuals can set aside cash on a pre-tax basis to spend for qualified medical expenses.

{kind=link}

Latest Posts

Evaluating the Best Rewards Cards for 2026

Ways to Boost Your Rating Quickly in 2026

Practical Techniques to Conserve Cash in 2026